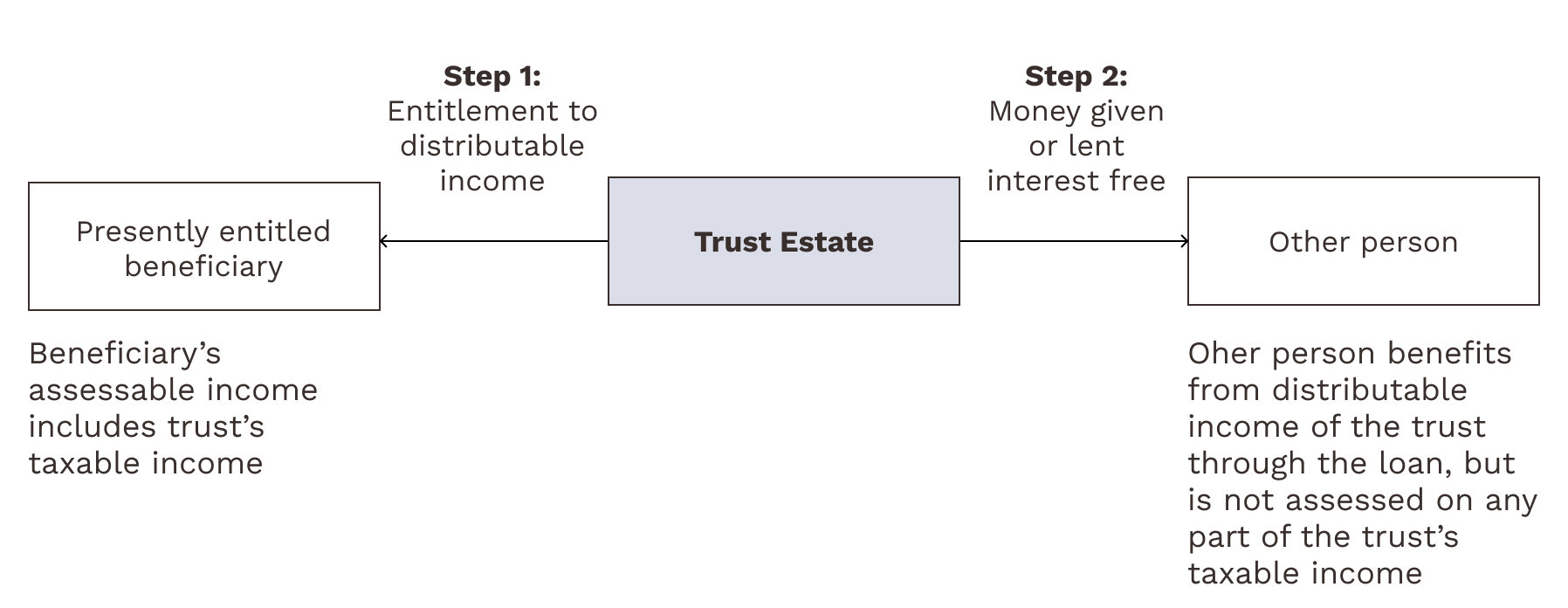

In late February of 2022 the ATO released a draft ruling under Section 100A (s100A) in Division 6 of the Income Tax Assessment Act 1936 regarding the treatment of ‘reimbursement agreements’ resulting from trust distributions. Broadly speaking a ‘reimbursement agreement’ is when a beneficiary of a trust (usually a child) is entitled to a distribution of income from the trust however the economic benefit (physical payment) of the distribution is received by another member of the trust (usually a parent).

What is the purpose of s100A?

s100A is an anti-avoidance provision the ATO enacted in 1978 to target certain reimbursement agreements that were happening at that time. Over the last 40 years the ATO has not been concerned about the normal family arrangements of distributing income within a family group. The ATO has now changed its position and is concerned that these reimbursement agreements lead to taxpayers reducing their income tax liability by distributing taxable distributions to beneficiaries who are not physically receiving the benefit of these distributions to access lower tax rates and tax-free thresholds. In the event the ATO determines that s100A applies than the distribution in question will be taxed to the trustee of the trust at the highest marginal tax rate.

What are the main areas of concern?

Whilst there is a comprehensive list of ways in which reimbursement agreements can take place in relation to trust distribution arrangements there are two key areas that the ATO has identified that are under the microscope:

- Trust distributions to adult children; and

- ‘Washing machine’ distributions.

Trust distributions to adult children:

In conjunction with s100A the ATO released Taxpayer Alert 2022/1 to provide clarity on the treatment of trust distributions to adult children. The view the ATO has taken is in the event an adult child beneficiary is entitled to trust income but does not physically receive this distribution this will lead to the application to s100A resulting in the trustee being taxed at the highest marginal rate.

The ATO has taken the view that such arrangements are typically used for the purpose of lowering the tax liabilities of those receiving the economic benefit of the trust and not to the children. Such arrangements have been common practice for a long time for small businesses with adult children on lower income thresholds whilst they are working part-time or attending further education after high school. It is important to note that as of writing this the ATO has considered that any income received by a spouse in such similar arrangements are not targeted as part of the s100A guidance.

‘Washing machine’ distributions:

A ‘washing machine’ distribution (or circular funds of flow) occurs when a corporate beneficiary of the trust becomes entitled to income at the end of an income year and pays tax at the corporate rate then subsequently pays out a franked dividend the following year back to the trust (as shareholder of the company). This process is often repeated over several years. The benefit of such an arrangement results in the trustee receiving a reduction in tax as the funds are only paid at the corporate tax rate and rolled from year to year. The ATO has taken a view that s100A would apply in such situations and the trustee would be liable to pay tax on the distribution amount at the highest marginal tax rate.

What happens next?

We are still in the early stages of understanding how and when s100A will be applied by the ATO. The ATO have released a draft practical guidance on types of arrangements where compliance resources will be utilised by the ATO to review such trust arrangements.

However, it is important to note that this guidance is still in the draft stage, and we would expect significant further information to come from the ATO over the next 12 months. At this stage the ATO have indicated that they will not be applying s100A retrospectively.

In the meantime, at Accura Accounting and Advisory we will be following this space very carefully as more information becomes available and whilst preparing your trust distribution minutes and income tax arrangements for the next income year, we will have conversations with each of our clients about the impacts of s100A with regard to their individual circumstances.