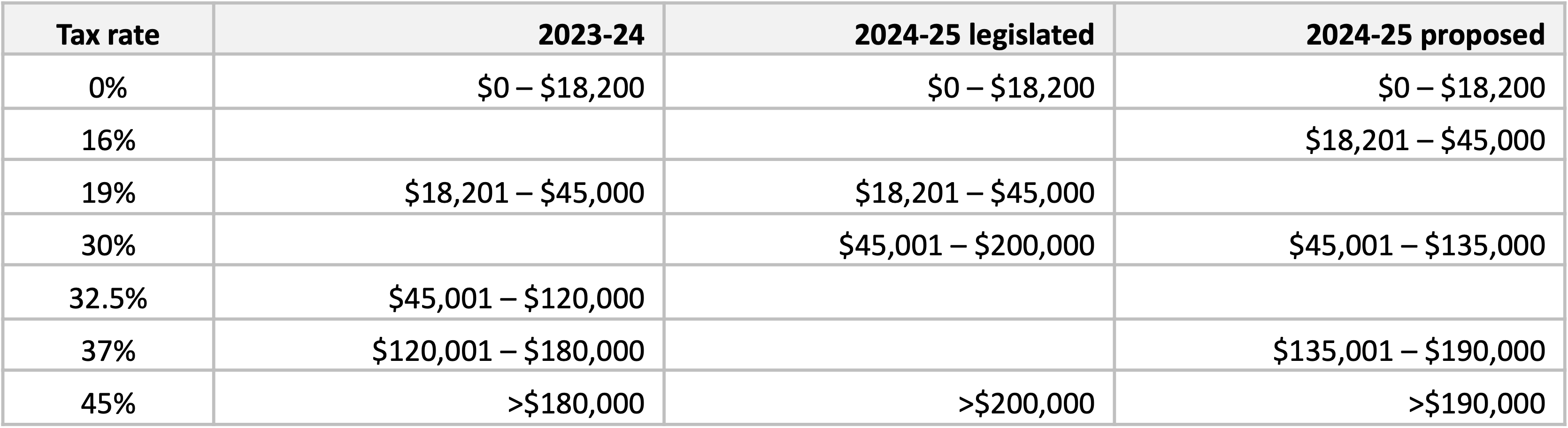

The personal income tax cuts legislated to commence on 1 July 2024 will be realigned and redistributed under a proposal released by the Federal Government.

After much speculation, the Government has announced that they will amend the legislated Stage 3 tax cuts scheduled to commence on 1 July 2024. This will mean that more Australian taxpayers will receive a personal income tax cut and take home more in their pay packet from 1 July, but for some, the impact will be less favourable than it would have been prior to the redesign.

What will change?

The revised tax cuts redistribute the reforms to benefit lower income households that have been disproportionately impacted by cost of living pressures.

Under the proposed redesign, all resident taxpayers with taxable income under $146,486, who would actually have an income tax liability, will receive a larger tax cut compared with the existing Stage 3 plan. For example:

- An individual with taxable income of $40,000 will receive a tax cut of $654, in contrast to receiving no tax cut under the current Stage 3 plan (but they are likely to have benefited from the tax cuts at Stage 1 and Stage 2).

- An individual with taxable income of $100,000 would receive a tax cut of $2,179, which is $804 more than under the current Stage 3 plan.

However, an individual earning $200,000 will have the benefit of the Stage 3 plan slashed to around half of what was expected from $9,075 to $4,529. There is still a benefit compared with current tax rates, just not as much.

There is additional relief for low-income earners with the Medicare Levy low-income thresholds expected to increase by 7.1% in line with inflation. It is expected that an individual will not start paying the 2% Medicare Levy until their income reaches $32,500 (up from $26,000).

While the proposed redesign is intended to be broadly revenue neutral compared with the existing budgeted Stage 3 plan, it will cost around $1bn more over the next four years before bracket creep starts to diminish the gains.

The current, legislated, and redesigned Stage 3 tax rates for Australian resident taxpayers

It’s not a sure thing just yet!

The Government will need to quickly enact amending legislation to make the redesigned Stage 3 tax cuts a reality by 1 July 2024. This will involve garnering the support of the independents or minor parties to secure its passage through Parliament.

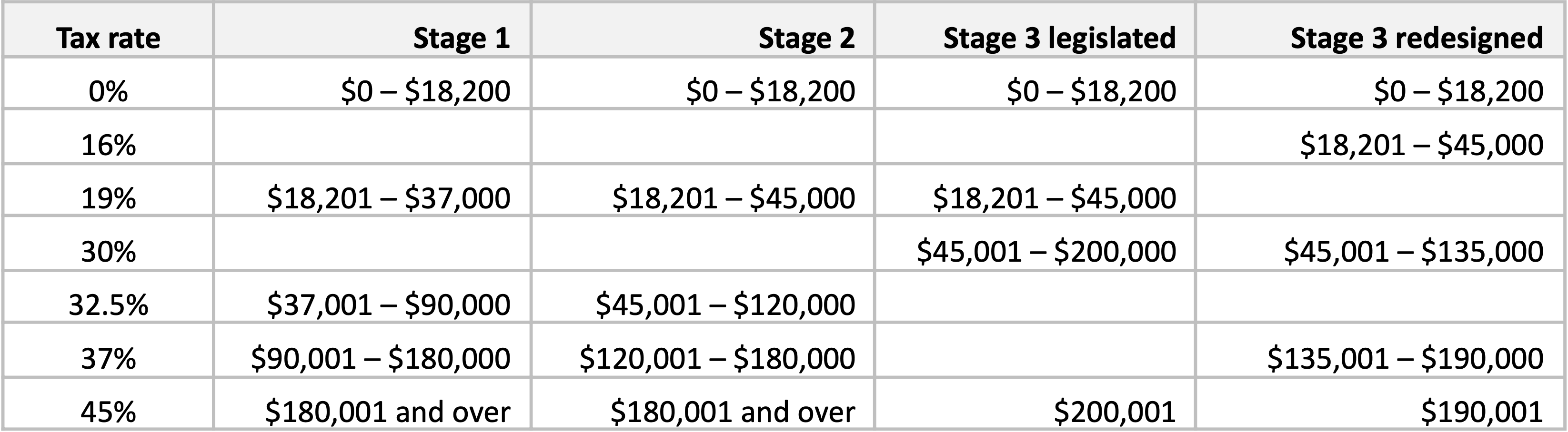

How did we get here?

First announced in the 2018-19 Federal Budget, the personal income tax plan was designed to address the very real issue of ‘bracket creep’ – tax rates not keeping pace with growth in wages and increasing the tax paid by individuals over time. The three point plan sought to restructure the personal income tax rates by simplifying the tax thresholds and rates, reducing the tax burden on many individuals and bringing Australia into line with some of our neighbours (i.e., New Zealand’s top marginal tax rate is 39% applying to incomes above $180,000).

The three point plan introduced incremental changes from 1 July 2018, 1 July 2020, with stage 3 legislated to take effect from 1 July 2024.

The three stages of reform

Any concerns?

If you have any concerns about the impact of the proposed changes please just give us a call.

Note: The information contained in this update has been provided as general advice only. The contents have been prepared without taking account of your personal objectives, financial situation or needs.

You should seek advice before making any decision regarding any information, strategies or products mentioned to consider whether that is appropriate to your own objectives, financial situation and needs.

Current as of 25 January 2024.

Limited liability by a scheme approved under Professional Standards Legislation.